The insurance industry is notoriously bad at customer experience. Not in China though. In the last few years, Chinese tech giants have been making massive strides at becoming the center of insurance innovation. Look at just one example: WeSure, the insurance platform emanating from the messaging app WeChat, celebrated over 55 million users on its second anniversary. This means that today, the biggest challenge of Chinese insurers is not just digitizing the business but going beyond traditional offerings and even merging insurance with other financial services. To compete, insurance companies revolutionize the industry using AI, IoT, and big data.

Customer satisfaction score (CSAT) and net promoter score (NPS) are the most important metrics for any insurance company. Yet, in the US, they majorly lag behind as insurers fail to keep up with expectations as other industries have risen. With the claim filing process being the biggest influencer of customer satisfaction, let’s look at the ways technology can bring revolutionary change to costs, operations, and customer experience.

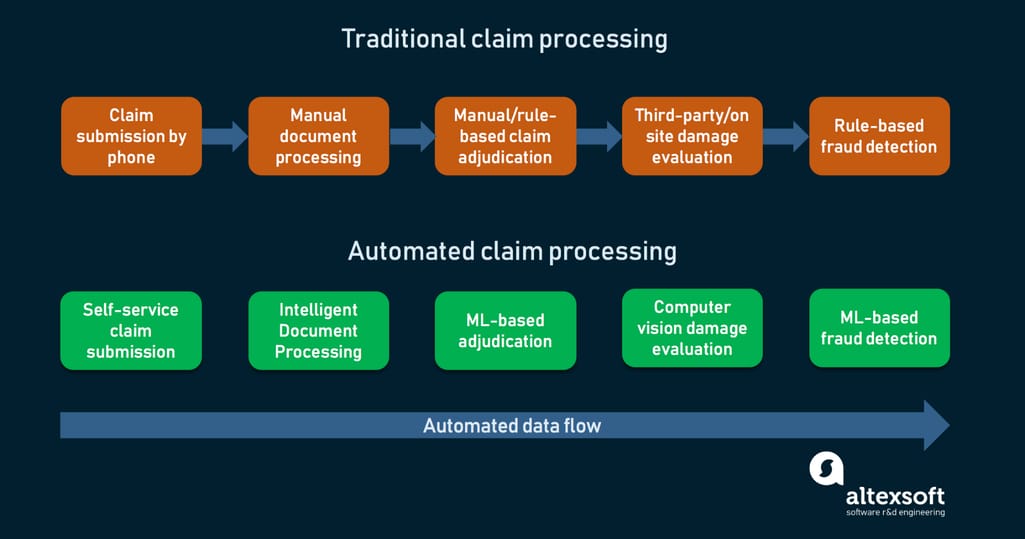

Why automate claims?

Why do insurance companies struggle with digitization and automation in the first place? If we set aside the typical reasons like the unwillingness for change among personnel or the lack of budget and technical resources, there’s one big reason that stems from the nature of insurance—insurance processes are usually too variable and unstructured to easily incorporate in the digital workflow.

For example, claims data exists in numerous formats (photos, handwritten documents, voice memos) and is shared via numerous channels (email, document attachments, phone calls, chats), making it extremely hard to receive and analyze with high accuracy without an agent’s personal attention. And when it comes to decision-making, it’s often more nuanced than an off-the-shelf system can handle—understanding the context of each individual case is required.

Does it mean that the insurance industry can never be automated and we need human input for every part of the process? Of course not. But it does need more advanced approaches that mimic human perception and judgment like AI, Machine Learning, and ML-based robotic process automation.

Outdated vs modern claim processing techniques

That’s where modern automation techniques come in. As Justin Lewis-Weber, CEO of an insurtech startup Assured, says, “Claims automation is really the Holy Grail of insurance. Fundamentally, it works on the three most important metrics that insurance companies care about: retention, expenses, and loss ratio. If we can solve the common pain points in claims through automation, then we can improve all three metrics dramatically.”

Let’s see where and how automation helps to improve the process. And we’ll start from the first point of contact between insurer and policyholder.

Self-service FNOL intake

The First Notice of Loss or FNOL is the first notification to the insurance provider that an asset was lost, stolen, or damaged. It’s a document that details the incident and damages, following the customer’s personal account of what happened.

Many insurance carriers still receive FNOLs by phone, and it often takes a long time for a call center operator to gather all information from the insured, usually with numerous follow-up calls.

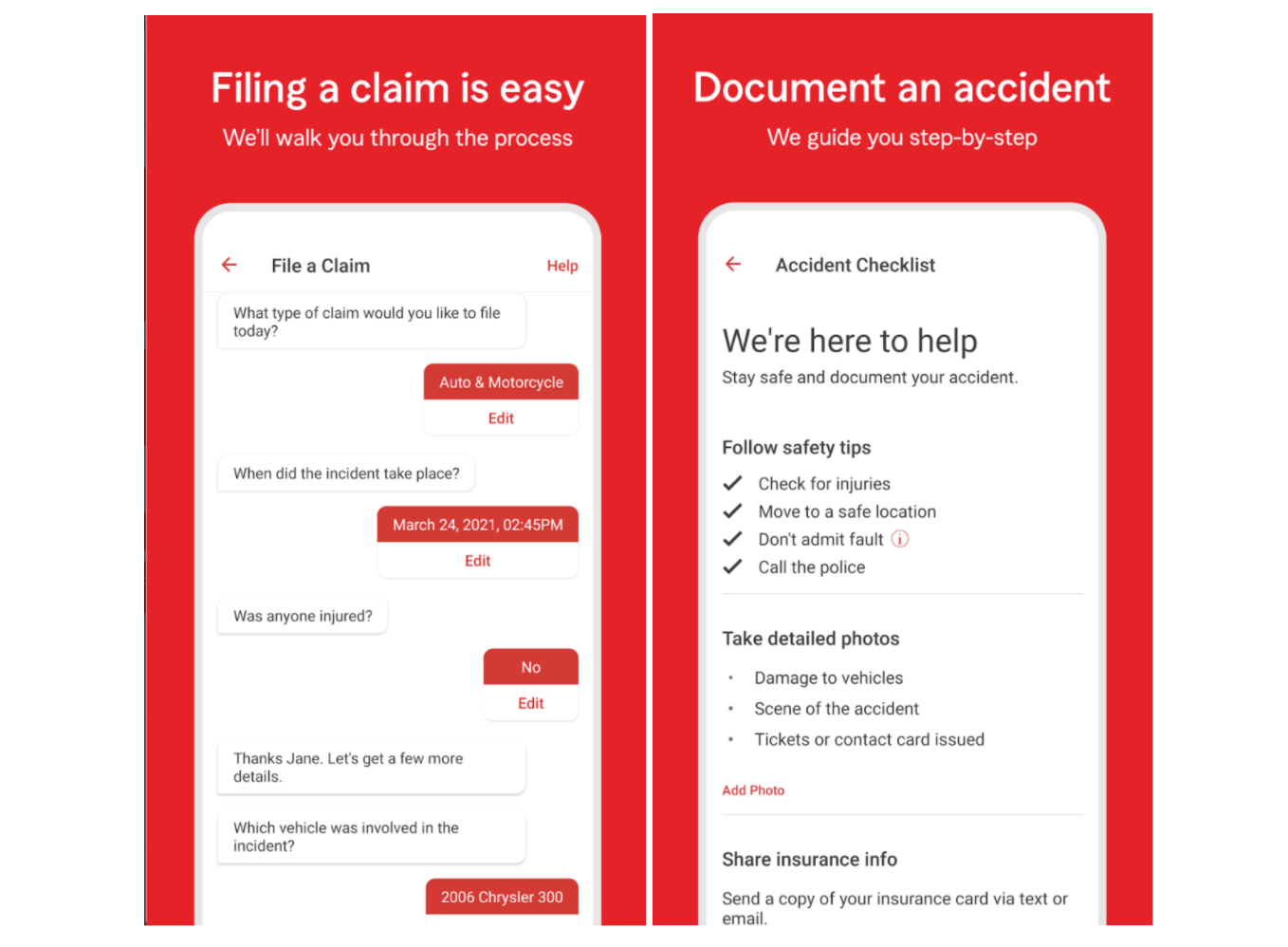

Today, electronic FNOLs are common, when instead of calling the insurer or handing the documents in person, the customer can use a chatbot or a mobile app to fill in the needed information, upload media files and document scans, allowing the insurer to handle claims faster and with better accuracy.

StateFarm uses a chatbot within their mobile app to help policyholders file a claim

How to implement digital FNOLs

An automated FNOL intake system consists of two components:

- a customer-facing interface (a web-based form, a mobile app, a chatbot in a messenger)

- a claim management platform that will receive and analyze claims

If you’re using modern claim management software, ask your provider what FNOL intake systems they have integrations with. Some, like Guidewire and Snapsheet, will have digital FNOL interfaces out of the box. If there’s nothing in their catalogs that suits you, you can pick a third-party digital FNOL intake system, like those from Capgemini and Wipro, and integrate their APIs using your own IT efforts.

If you’re relying on a legacy system for your operations and don’t have resources for complete modernization, you can still connect with FNOL intake providers using an older EDI connection, such as Netsmart or OneShield. Also sometimes, the cheapest and most effective option would be building your own FNOL intake capabilities that fit your workflow the best.

Digitized and structured FNOLs are integral to the automation success of the business and in the following sections, you will see it. But although eFNOLs provide better customer experience, they may not be particularly helpful to insurers who still need to follow their regular workflow of digitizing handwritten documents and photographic evidence, transcribing audio and video reports, and contacting customers for missing information. Let’s look at solutions to these problems.

Intelligent Document Processing

For decades, organizations have been using Optical Character Recognition (OCR) to process physical documents, basically converting handwritten and printed text into machine-encoded text. Although delivering extreme accuracy for typed text, OCR uses manually created templates and can make small mistakes in crucial information, like someone’s name, the date, or the price, that will render the digitized copy useless. This means that files processed using traditional OCR should be reviewed manually, which is a far cry from automation.

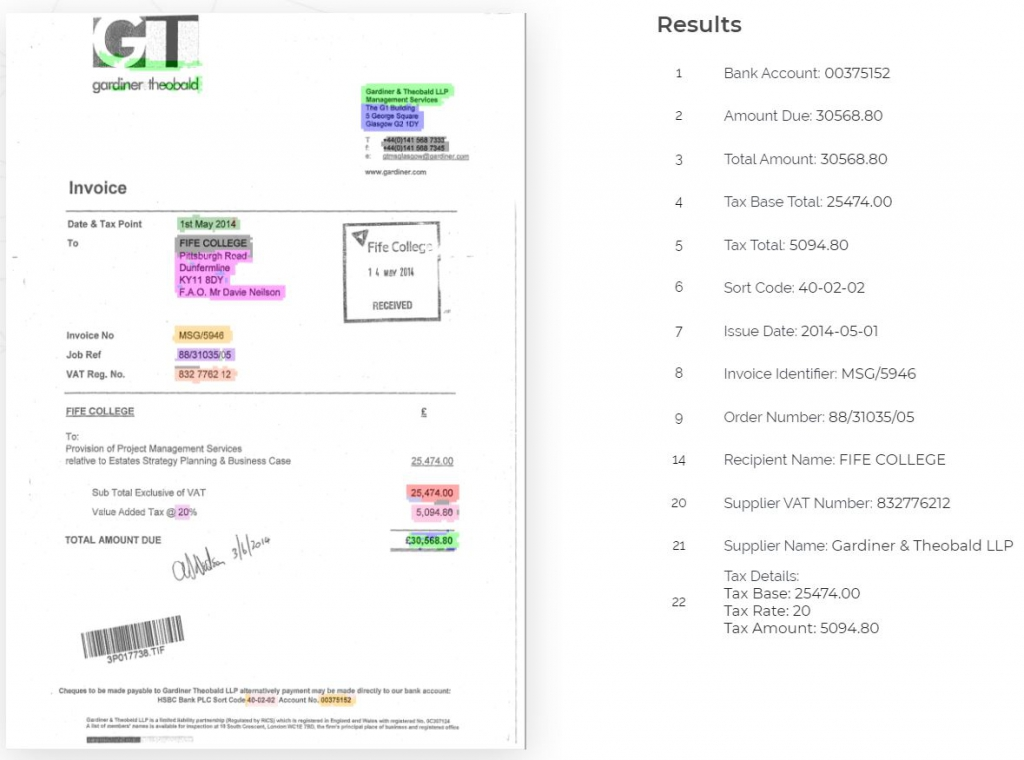

A modern alternative to OCR is Intelligent Document Processing (IDP), which is also called Cognitive Document Processing (CDP) or ML OCR. This AI-based technology uses natural language processing, computer vision, and deep learning to improve document quality, classify docs, and extract unstructured data that can then be converted into usable, structured data.

Neural networks correctly extract data from an invoice. Source: Rossum

IDP is commonly complemented by robotic process automation, which allows automating many typical business tasks using predefined workflows. For example, an RPA bot using IDP can analyze documents sent by the customer, extract relevant data from text and media, and send it for further processing, like manual review or fraud detection algorithms, all without human intervention.

How to implement IDP

Intelligent Document Processing usually functions on top of an RPA software. Read our article where we discuss RPA implementation options separately. A good thing about IDP systems is that they don’t have to be targeted to the insurance business and the provider options are broader. Depending on where you’re at, you have two implementation options.

Employ an ML-based RPA system. Solutions such as UiPath or Automation Anywhere have their own cognitive document processing capabilities and require minimal integration effort on your part.

Implement third-party IDP. Whether you want to complement your existing RPA activities or upgrade traditional OCR you’ve been using, consider such providers as Appian, InData Labs, or insurance-focused Infrrd.

Read more about how IDP works in insurance in our dedicated post.

Smart claim triaging using predictive analytics

Claims triage is the process of sorting high volumes of claims by urgency. In case of catastrophic events or simply during peak season when insurers are experiencing large claim intakes, they need to quickly and confidently identify which claims need to be resolved first and by whom. Here’s where predictive analytics can come in handy.

Based on historical data, predictive analytics uses statistics and machine learning techniques to identify the likelihood of future events. Because of all the data about accidents carriers collect and store, they can apply predictive analytics to distinguish light claims that can be automatically accepted from complex claims that need to be appropriately adjusted.

Here’s how it usually works, according to Genpact.

- Using digital FNOL intake channels, claim data is collected and structured.

- Each claim is assigned a complexity/urgency score based on parameters from similar historical claims: injury severity, damage extent, degree of suspiciousness, litigation potential, etc.

- Based on the score, claims are segmented and routed to appropriate adjusters based on their experience and/or workload.

- Low complexity claims are sent straight to payments.

How to implement predictive analytics

You’re probably using some kind of analytics already. (Use our article to determine your stage of analytics maturity.) But predictive analytics requires a lot more investment than its previous iterations.

Introduce analytics technology. Get integrated data management tools, such as BI dashboards and data repositories, that allow non-technical people in your company to access insights and make decisions.

Foster a data-driven culture. People will be able to use those tools only when they’re embedded into their existing workflows and reflect their needs. For this, make sure to provide training to your staff so they know where and how to find data insights.

Hire machine learning specialists for the team. Employ data science professionals who will drive automation by creating data pipelines, building models, and integrating technologies.

FNOLs, however, don’t have to be the only sources of immediate data about claims. Internet of Things devices are a valuable source of real-time data that can help expedite the claim management process.

Telematics and IoT for better data accuracy

Internet-connected products such as water sensors, smoke alarms, or in-car sensors provide a massive amount of information—and subsequently, insight—for insurers.

Homeowners in the US file over 14,000 water damage claims per day, with an average cost of up to $15,000. Not only can this damage be prevented using alerts from sensors, resulting in lower numbers of claims, but data from these sensors can be applied to predictive analytics models and help adjudicate such claims much more quickly.

Data from IoT devices can also automate FNOL submissions. Not only can sensors assess damage more accurately than the insured, but they can also do it instantly. In case of car accidents, telematics data about speed, braking, the direction of impact, and more will detail the actual turn of events and speed up adjudication and fraud detection.

How to implement Internet of Things

As described in detail in our article, an IoT system consists of four layers:

- Perception layer or the things themselves

- Connectivity layer that transfers data from devices to the cloud

- Processing layer that manages data streams

- Application layer where reporting and device control happen

The infrastructure is handled by IoT platforms such as Cisco IoT, AWS IoT Platform, or Microsoft Azure IoT. You can review our comparison to make a choice.

But you will also have to handle the perception layer—which devices you will use and target. The simplest solution would be establishing a partnership with a device manufacturer and offering sensor installation as part of your service. See the examples of HSB, Progressive, and Hippo.

Damage evaluation using computer vision

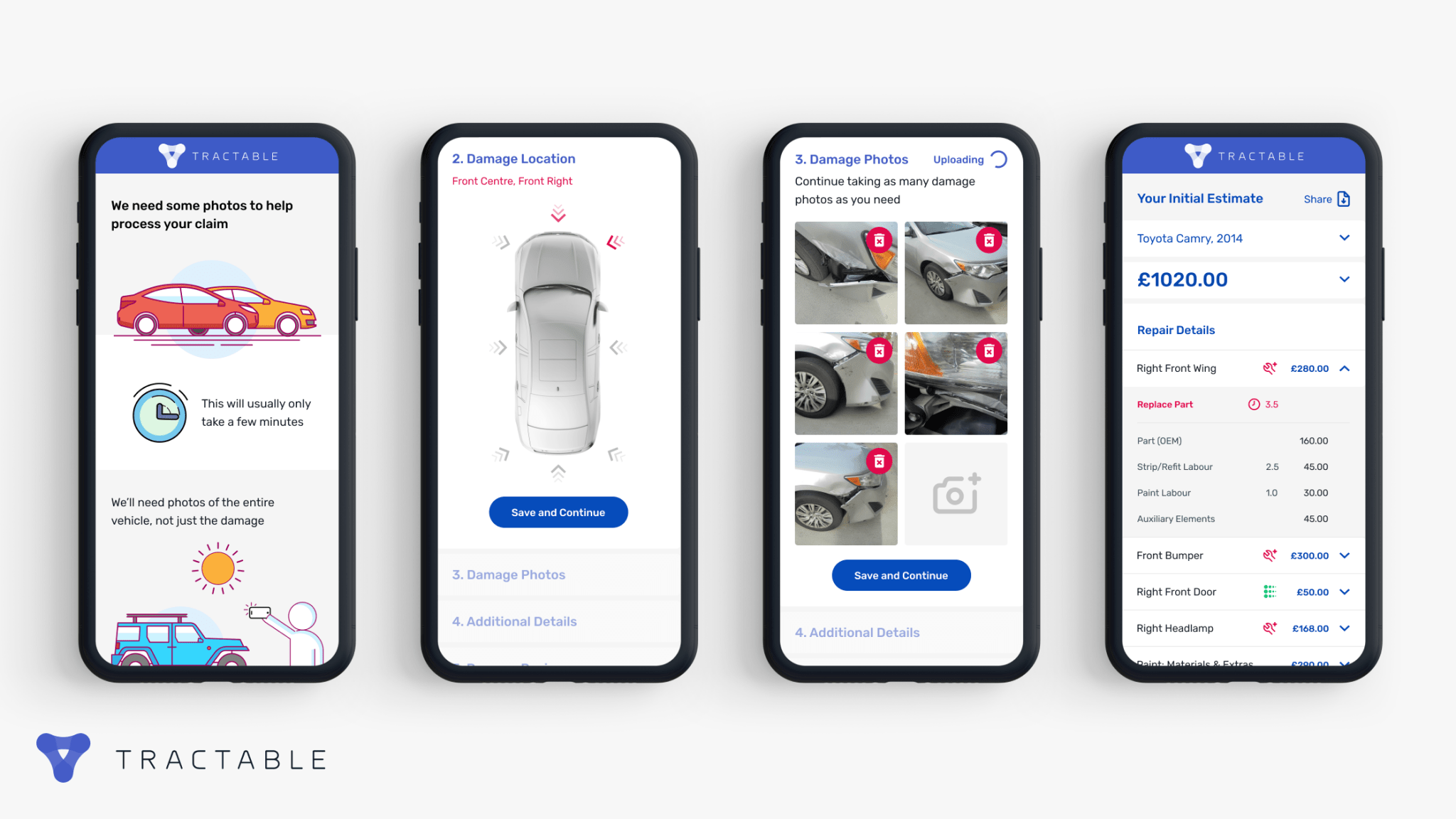

In typical situations, damage estimation is handled manually in a vehicle repair shop and/or by an adjuster arriving at the accident site. It takes days, if not weeks, to receive a report from an expert, which in turn has to be inspected by an insurance provider for mistakes or unfair payouts. Instead, the machine learning model can compare the smartphone image to its vast database of car damage pictures to determine the severity and estimate the cost of the repairs.

A leading insurer Ageas uses technology by Tractable to evaluate vehicle damage. Source: Tractable

Besides auto insurance, computer vision can help process property claims, for example, after a disaster. Take roof inspection after a storm—not only is it not safe but also time-consuming with numerous parties and various equipment getting involved. So, drone inspections with automated damage detection are becoming more and more prevalent. Drone inspection providers such as IMGING, Kespry, and Loveland use AI-driven image detection tools to generate detailed and precise roof wireframes and highlight damage on the images.

A similar process can be scaled to assess whole territories for crop insurance. Although there are currently no cases of agriculture claim validation using such methods, drone and satellite imagery are currently used for field analysis. This means that the same datasets can be used to build image detection models and provide the most precise loss estimations.

How to implement computer vision

Computer vision for insurance use cases will be different from other applications, so you will need a specialized provider who has acquired large datasets of damages and disasters to rely on.

Other components are also important. For auto insurance, you want image recognition functionality embedded in a mobile app. For property insurance, you have to figure out if you should buy drones or outsource it to someone. Vendors like Cape Analytics, Tractable, and Nexar provide an end-to-end functionality and integration to your system.

But as usual, you can do custom development. With the help of skilled data scientists, you can take tons of publicly available damage data as far back as historical data you collect and train neural networks on it. Or you can use off-the-shelf image recognition products from Google, Amazon, IBM, or Microsoft.

Auto-adjudication

Claim adjudication refers to the process of paying or denying insurance claims by reviewing the claim’s correctness and validity. Typically done by the insurance company staff, adjudication includes a long list of checks: for errors or omissions, for the appropriate diagnosis or procedures, for the correct insurance policy, etc.

Since many of these checks don’t require human intervention and are highly repeatable, this process calls for automation. There are two types of solutions you can consider.

Rule-based auto-adjudication

Using so-called business rule engines, insurance companies create business rules that are then applied to calculate a claim’s eligibility instantly. Such engines can work with a certain level of complexity and analyze criteria at multiple levels, as long as the data for it is mapped correctly and the handling logic is modified when it’s needed. As rules are often written and read in human languages, you can operate such an engine without constant tech support, but its functionality is limited to your idea of possible business cases and the ability to correctly map and update the information. But at some verification stages, you might want to consider more advanced methods.

Claim adjudication using both business rules and ML-based technologies. Source: QBurst

ML-based auto-adjudication

Some of the areas where rules fall short are that they can neither review nonstandardized documents and images, nor can they capture sophisticated fraud . This is where human employees are typically needed. However, these steps can also be automated.

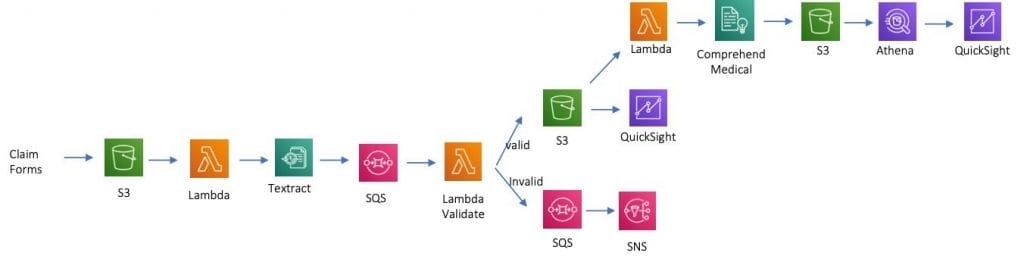

The first task is information extraction. Instead of having officers read through pages of lab results and review images, a machine learning model can use computer vision and natural language processing to extract data from such sources and then send them to the rules engine to perform standard analysis. Look at the example using Amazon Web Services—an MLaaS platform for handling all types of AI operations.

ML-based automation can augment business rules and be applied only when needed. Source: Amazon

The architecture of this workflow describes the process of storing claim documents, extracting entities and relationships from them, then validating extracted instances, which, if validated, are further stored, and if not, result in notification to the user. Then, Amazon’s Comprehend Medical system extracts medically relevant information from the claim forms, which is then analyzed against the clinical procedure and finally visualized on the dashboard.

The second task is fraud detection, which we will cover in a separate section.

Fraud detection

Insurers estimate that around 18 percent of all claims are fraudulent. Fake accidents and vehicle thefts, along with phantom medical procedures, are some of the most common types of claim fraud. Although you can create rules to make checks for well-known indicators of fraud, you will have nothing to combat newly appearing schemes or fraud patterns unnoticed by human analysts.

A machine learning algorithm will analyze FNOLs, police reports, medical bills, forms filled by clients and insurance agents, will find correlations that may be missed, and will do this instantly, in real time. And when a claim is flagged as potentially fraudulent, depending on the probability, the payout can be automatically denied, or human agents can investigate the claim further.

Building and testing a fraud detection model. Source: Wipro

How to implement ML for claim verification

We supplied an implementation hint above—Machine Learning-as-a-Service platforms. MLaaS has tons of applications. Solutions from Amazon, Google, IBM, and Microsoft have tons of products for your business needs. And although they exist to simplify ML development, the choice may be overwhelming, especially if you don’t have data science expertise in-house. We can give two recommendations here.

Pick a single problem. Choose the type of claims you have to deal with the most and write a schematic workflow: where data comes from and where it goes, who reviews and validates information, and what happens to it next. Then match those operations with MLaaS solutions and pick the ones that can solve those problems best.

Hire a data scientist. Employ someone versed in MLaaS implementation and test your first automated workflow for efficiency. If the results exceed the effort, continue with your next problem.

The success of ML activities depends on the availability and quality of the needed data. For insurers that collect tons of data every day, the former parameter shouldn’t be a problem. The latter one might pose issues. Let’s talk about these and other challenges of claim automation.

Claim automation challenges and solutions

Insurers are cautious about automation and it’s understandable. Yet, the general advice is to start small and choose one operation that you feel would bring the most benefit before you move on to full-on transformation. Just remember to prepare to tackle the common obstacles you will face on the way.

Siloed data

Data silos are not an insurance-specific problem, but they're relevant in organizations that are used to “doing business the old way.” There, departments work independently and rarely share data, not always because they don’t want to, but because they have no means to, each existing on a different digital page.

How to break down silos? The silo problem is spawned when each department starts using its own data management system and creates a logic that only they understand. So, the first step would be implementing a company-wide data inventory. Of course, this is a task for data integration experts, but this is the only way to build a strong, common foundation for your future analytics.

Skill gaps

As you discover more opportunities for automation, you will have to find better tasks for your existing workforce. Operations are usually hit the hardest, with many employees losing jobs due to a lack of other skills or planning from the company.

How to retain the workforce? Identify imminent skill gaps and either find people in your company to fill the positions or hire. Provide training to the staff to help them adapt to new processes faster and succeed at them.

Legacy infrastructure

We’ve talked a lot about the harm legacy software does to organizations. High maintenance costs, lack of security, and losing to more efficient competitors are but a few. But the worst flaw is stagnation since ancient systems can no longer support integrations crucial to business growth.

What to do with legacy software? There are different routes you may want to go, which you can find at the link above, but start by employing a great IT team. Professionals will be able to assess your current situation and suggest the best scenario for your budget and time constraints.

Maryna is a passionate writer with a talent for simplifying complex topics for readers of all backgrounds. With 7 years of experience writing about travel technology, she is well-versed in the field. Outside of her professional writing, she enjoys reading, video games, and fashion.

Want to write an article for our blog? Read our requirements and guidelines to become a contributor.