The 2022 Juniper Research BNPL study calculated that there are currently around 360 million users of the “Buy Now, Pay Later” programs. By 2027, this number is expected to reach 900 million. Another survey, conducted by C+R Research, states that 60 percent of online shoppers have tried the BNPL service.

These and other market stats show growing consumer interest in alternative payment methods to credit cards. Once applied mostly to finance big purchases such as furniture, electronics, or vacations, today BNPL is becoming so widespread that apps actually offer to pay in 4 installments over 6 weeks when ordering snacks!

It’s pretty clear that businesses have to catch up with the trends and offer their customers the desired payment options. In this post, we’ll discuss the BNPL approach in the travel industry, talk about the main BNPL providers, and look at how businesses can implement the service and benefit from it.

The Rise of Buy Now, Pay Later in Travel

What is buy now pay later?

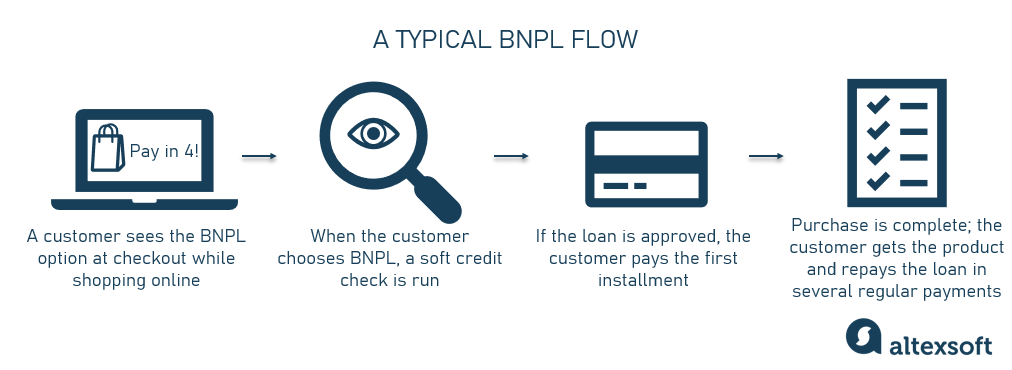

Buy now, pay later or BNPL is a type of short-term credit that allows shoppers to divide their purchase into multiple smaller payments. The first one is usually duе at checkout, while others are paid on a weekly, biweekly, or monthly basis. A common structure includes a total of 4 payments (that’s why BNPL is often called “pay-in-four”) stretched over 6 weeks, but it can vary.

Since BNPL is essentially a loan, customers undergo a soft credit check. As for commissions, such installments are often interest-free for shoppers. However, if a borrower misses a payment, a late fee is charged (usually, $5-15) – and that’s not like it happens once in a blue moon. Actually, studies show that 42 percent of BNPL users have failed to observe their payment schedule.

In retail, shoppers get their purchase immediately after the first installment is credited, but if BNPL is used to buy services (travel, insurance, education, etc.), the consumer often has to pay it off before they get the service. A typical example is a layaway vacation or flight booked way in advance but that has to be paid in full before the departure date.

A typical BNPL flow

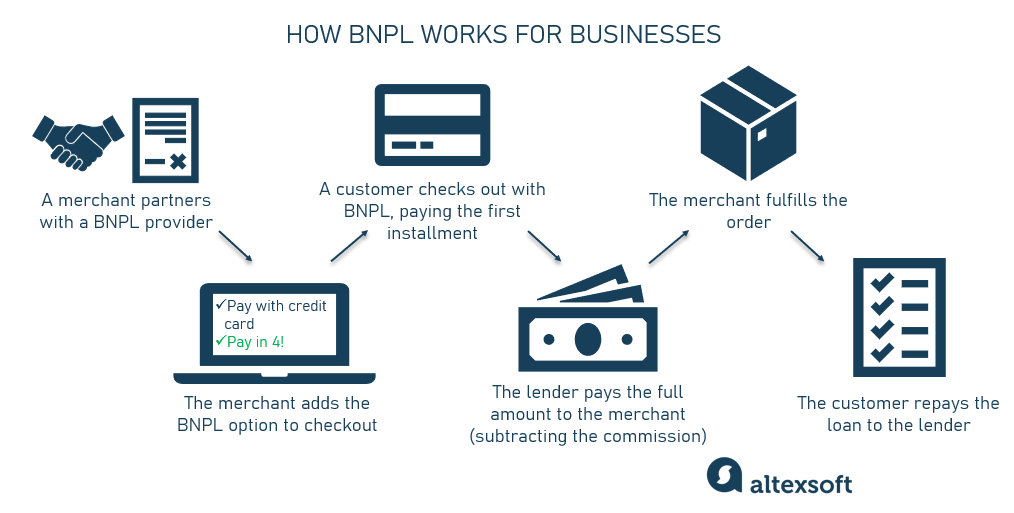

How buy now pay later works for businesses

If a company wants to offer its customers a BNPL option, it has to partner with a third-party service like Klarna or Uplift (we’ll discuss them in more detail further on). BNPL providers usually charge their partners a commission – but they are the ones that take the risk of nonpayment.

By the way, the same relates to currency exchange rate fluctuations (which is important for travel businesses as they often deal with international customers). As a rule, a BNPL lender takes the risks (and benefits) of currency rate instability (when selecting a provider, check their policies regarding this).

When customers complete the checkout and pay down the first installment, the BNPL provider transfers the total value of the purchase to the merchant and then collects the rest of the sum from the customer as the latter repays the loan. In the case of refunds, the process is similar to the traditional credit card refund procedure, but the fees are usually not compensated.

A typical BNPL flow from a business perspective

BNPL benefits

So why is BNPL good for customers and merchants alike (not to mention lenders that make money off it)? Here are the main reasons.

BNPL is convenient for shoppers as it allows them to

- afford bigger purchases,

- lock in the best price,

- avoid credit checks and credit card interest,

- free up cash flow, and

- grab the high-demand product or service before it’s sold out.

Also, it’s often the only way to cover unexpected or emergency expenses.

On the other hand, businesses profit from the BNPL payment option as it attracts more customers and often encourages them to buy more than they have planned, driving upselling and leading to incremental sales (actually, 59 percent of BNPL users admitted that they purchased unnecessary items beyond their means). BNPL is especially beneficial for businesses selling high-value items – and the travel industry is just that, so let’s see how it works there.

Who would say they were never tempted? Source: imgflip

BNPL in the travel industry

Today, many travel businesses offer BNPL to their customers: from major airlines (see the offerings of British Airways, United Airlines, or Delta Airlines) to travel agencies (Expedia, Booking.com, or Get Away Today) to vacation rental companies like Vacasa. And for a reason.

The recent Amadeus Pay when you fly study discovered that 40 percent of respondents are more likely to book a vacation if they are given a BNPL option. Moreover, Tom Botts, chief commercial officer of BNPL firm Uplift, shared with CNBC that consumers “tend to spoil themselves when they can pay in installments. We see them buying premium economy or even first class [tickets] when typically they would not have bought.”

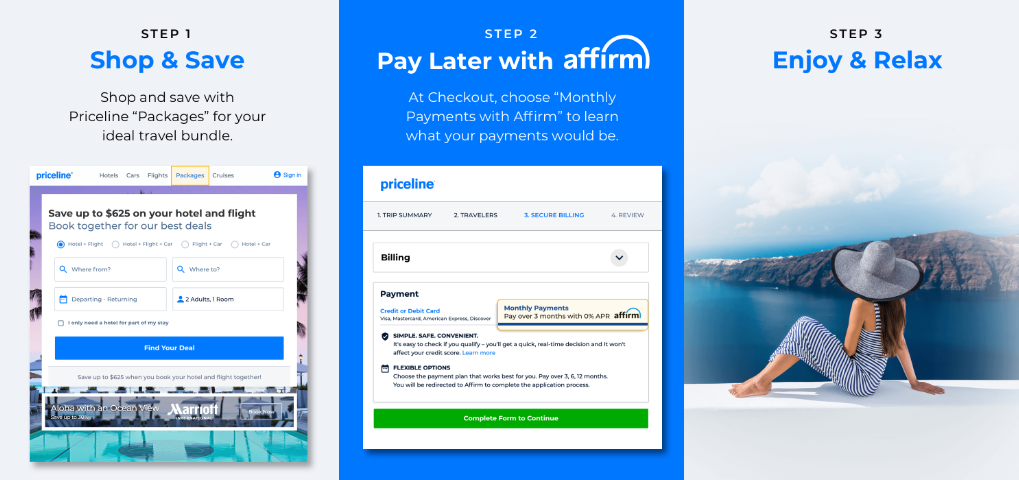

A short and easy BNPL instruction from Priceline

So if you as a travel business owner or revenue manager consider adopting BNPL to get a competitive advantage and increase customer reach, here’s what you have to do.

How to implement BNPL

Before your customers can see the sought-for BNPL payment option on your booking website, you have to jump through a few essential hoops.

Choose a provider

There's certainly an extensive range of BNPL service providers on the market today so the choice may seem somewhat intimidating. We’ll describe some of the popular BNPL lenders in the next section, but before that, you have to know the key comparison criteria to pay attention to.

Industry of focus. You can see some big names that work with multiple industries (like Klarna or Affirm), but there also are the ones that focus solely on the travel sector (e.g., Fly Now Pay Later).

Commission structure. There are two main types of plans:

- Merchant transaction fee loans. In this case, you as a merchant pay commission to the BNPL service provider – typically somewhere between 3 and 6 percent of the purchase amount. In addition, some BNPL lenders charge a small per-transaction fee (like $0.30). This option is more common since it’s interest-free for end customers – and thus more appealing for the shopper, so merchants choose it to “buy” client satisfaction and increase order value.

- Shopper interest loans. Within this plan, a customer pays interest, while you don’t pay any commissions to the BNPL lender. It might seem a better option for you but it obviously attracts fewer customers, so at the end of the day, the profit is usually smaller compared to the first plan.

Most BNPL lenders operate on one of these models, so carefully calculate the ROI and decide whether commissions are worth paying to increase sales volume.

Fees. A common merchant’s concern regarding BNPL is the pretty penny that you have to pay to the provider as the fees are usually bigger than the ones for processing credit card transactions. But as we said, there are lenders that don’t charge merchants. And even if they do, it makes sense to consider it as a cost of customer acquisition and increasing the sales volume. In any case, the fee structure and amount is an important factor to consider.

Preintegrated payment partners. If you want to add BNPL as a checkout option, you have to integrate it with your payment processing solution. Many big lenders come preconnected with major eCommerce platforms, point-of-sale providers, and payment gateways. For example, if you use Stripe, you won’t have any implementation problems with, say, Klarna or Afterpay as they have this integration out of the box. So when choosing a provider, it makes sense to prioritize the ones that have your payment technology among their partners.

Security. Fraud is another common reason for anxiety in any financial matters. Generally, BNPL fraud schemes are similar to credit card schemes. So what you can do is choose a reputable BNPL lender, giving preference to the bigger, more stable ones. We advise looking into their security procedures like fraud checks and customer vetting process, as well as PCI DSS compliance. Also, just like with any other payment method, your own online payment solution must have a high security level to prevent fraudulent activity.

Learn more about fraud detection from our video explainer

Choose a partnership model

Speaking of partnership models, we can distinguish two main cooperation options.

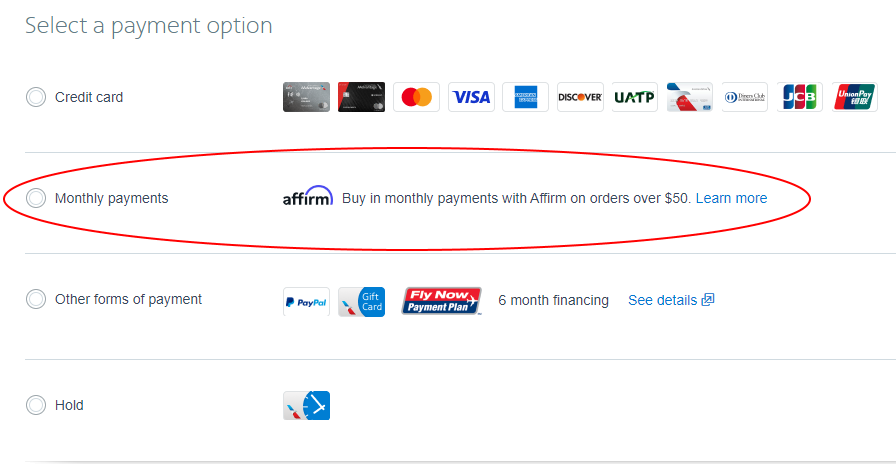

A merchant-partner model, being a more common one, involves implementing the BNPL payment option into the checkout stage on your website (well, it goes without saying that you have online booking functionality with payment processing). Most BNPL lenders also have online portals to handle payments that you receive offline.

Final stage of checkout at American Airlines

The downside of this approach is that you’ll have to integrate the new payment functionality into your existing checkout flow – which might take a bit of effort depending on the technology you have and the provider you choose.

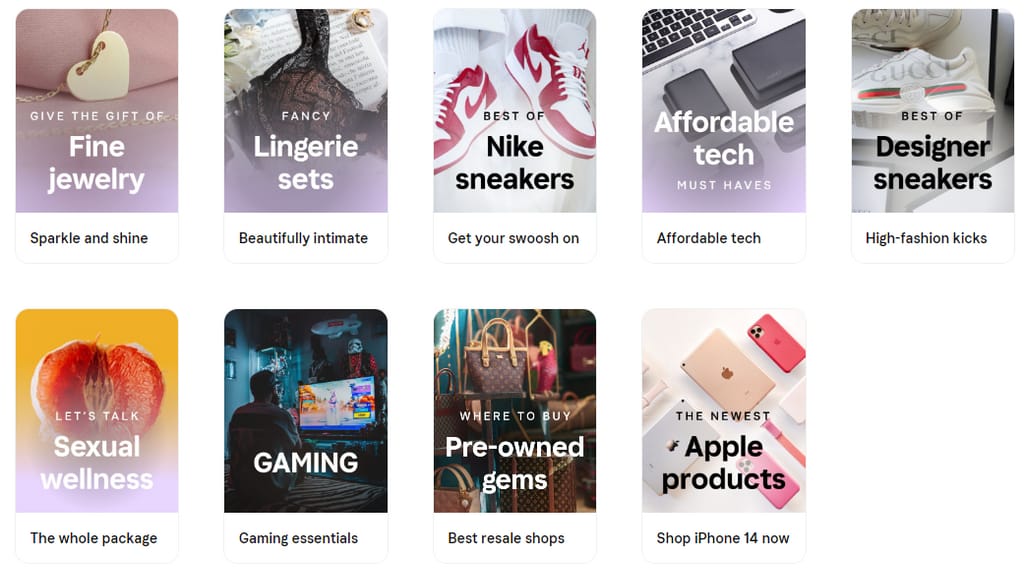

A BNPL app model entails the lender adding your products to the virtual shopping mall that consumers can access through its proprietary application. Such apps host a catalog of diverse brands from apparel and cosmetics to home appliances, video games, cars, and travel products that registered users can buy on a BNPL basis from a single interface.

Some of Klarna’s website offerings

Some providers only display their partners in the app and then redirect shoppers to the merchant’s website, while others offer in-app booking. To make it possible, lenders build an integration to pull the information on your inventory, availability, and rates from your database.

Most big providers offer both cooperation models. For a travel business, the first model is preferable since travelers usually go to a dedicated website in search of vacation options rather than book a trip in passing while shopping for new sneakers – well, unless it’s a travel-focused app like Fly Now Pay Later. However, you can certainly go with both of them, just be sure to discuss all the terms and conditions with a provider.

Apply for partnership

Once you find your perfect (or at least adequate) partner, you’ll have to fill out the application, submitting some basic details on your company. To make this world a bit more equitable, not only consumers go through a vetting procedure. Merchants also have to meet certain requirements to qualify – which is understandable since all financial institutions are required to adhere to KYC/AML regulations.

But worry not. Most BNPL lenders will welcome you as a partner since the travel industry is not among the ones that aren’t eligible (as are tobacco, gambling, weapons, sex products, and other closely monitored and/or questionable ventures).

Integrate

The complexity of integration will depend on the partnership model you choose and also whether the lender is preconnected with your payment technology. If you, as most businesses, opt for a merchant-partner model, you’ll most likely have to build an integration from scratch, so be prepared to engage IT specialists to develop it properly.

Anyway, all BNPL providers have a stake in your cooperation, so rest assured they’ll do their best to facilitate and expedite the integration process. All of them have a set of open APIs to link to your payment system, and if you choose to showcase your travel inventory in their app (the BNPL app model we talked about), they’ll even do the integration themselves.

Okay, so now that you have an idea about the implementation process, let’s finally explore the main BNPL providers.

Key BNPL companies servicing the travel industry

We’ll give a brief description of the major players so that you can compare them side by side and hopefully get a better idea of what to choose. We’ll go through the main comparison criteria listed above except for the security aspect since all of them are fully compliant and provide top-notch data protection when processing transactions.

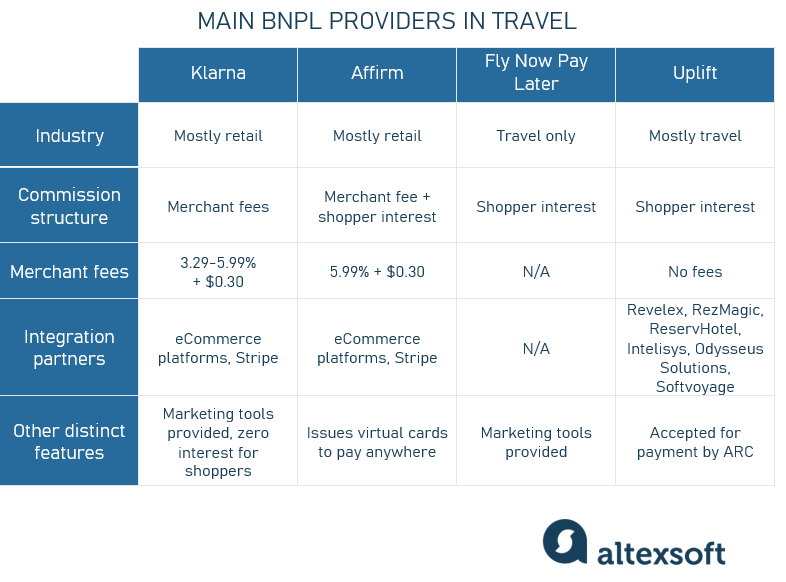

Main travel BNPL providers compared

Klarna: the biggest industry-agnostic provider

Klarna, a Swedish fintech company, is the renowned world leader in BNPL services with 150 million active users in 45 countries and 450,000 merchants. It provides shoppers with 3 installment plans (usually, interest-free), runs its own rewards program, and offers special deals on selected products.

Klarna places the strongest focus on retailers from apparel, beauty, electronics, and home goods vendors. As for the travel industry, it partners with Expedia, Viator, Trip.com, Alternative Airlines, and so on. However, the list of available merchants depends on the shopper’s location.

Commission structure. Klarna charges the merchant, while most payment plans are free for the shopper (late fees are charged though).

Merchant fees. Klarna’s fees include the percentage from each purchase (3.29-5.99 percent depending on the installment plan a customer chooses), plus the fixed $0.30 fee for each transaction.

Integration. To add Klarna’s service is easy if you use the platform of one of its eCommerce partners (which probably isn’t your case since travel businesses rarely build Shopify websites) or Stripe. Otherwise, they have a set of REST APIs and a developer portal with all the necessary documentation and instructions. You can also test its functionality before committing to a full-fledged integration.

Where to start. After integration and initial setup, you get access to the Merchant Portal to track all the orders and transactions. Klarna also offers marketing solutions to promote the BNPL payment method on your platform.

Affirm: issues virtual cards for installments

Affirm is a US-based financial company that offers short-term consumer loans to US shoppers. It boasts cooperation with over 245,000 merchants from different sectors, from retail giants like Amazon, Walmart, and Nordstrom to travel providers such as Expedia, Alternative Airlines, American Airlines, Delta Vacations, etc.

Besides, through the Affirm app or website, consumers can get a virtual credit card and make use of the BNPL option at any retailer, either online or in-store, that’s not on the Affirm’s partner list.

Commission structure. Affirm charges both merchants and shoppers for using the service. For consumers, the interest rate varies from 0 to 30 percent, but no late, annual, or other hidden fees are charged.

Merchant fees. Their fees range from 2 to 6 percent of the purchase price plus a $0.30 transaction fee, but the exact amount can vary by business type and size.

Integration. Affirm partners with all major eCommerce platforms and Stripe for effortless integration. Its REST APIs are available at its Developer Portal. You can also opt for a telesales integration or a single-use Affirm virtual card issuance.

Where to start. Here’s a link to create an account with Affirm which will then grant you access to the Merchant Portal where you can view transactions, monitor activity, and get your API keys. You’ll be able to choose the payment plan available to your customer, set up a minimum purchase amount, and so on.

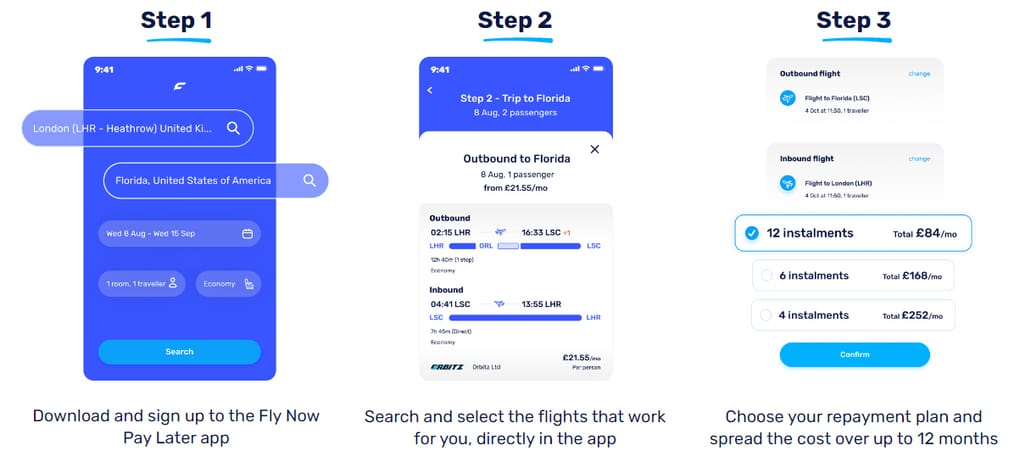

Fly Now Pay Later: a travel-focused app and checkout option

Fly Now Pay Later is a British platform designed specifically for travelers looking for BNPL deals. It’s now present in the US, UK, and EU markets. Fly Now Pay Later offers in-app booking. If you want to add it as a payment option, this lender issues a virtual credit card that allows shoppers to pay in installments.

Fly Now Pay Later in-app booking flow

Travelers can book diverse package holidays, hotels, flights, attractions, and cruises via the app (no desktop version available). In addition, Fly Now Pay Later continuously expands its list of partners who add the BNPL payment method backed by this lender to their online checkout (e.g., TravelUp and Alternative Airlines).

Commission structure. On its loans, the lender charges customers 0 to 42.4 percent interest. Information about merchant commissions is not disclosed.

Merchant fees. The information is not publicly available, contact them directly for details.

Integration. To add the Fly Now Pay Later payment option to your checkout, you can go with either their ready-made widget or APIs. The former is very easy to implement, while the latter means building integration from scratch. You can get more information about Integration in their portal.

Where to start. To register, contact their sales team. When you have an account, you’ll be provided a Marketing toolkit to inform your customers of the flexible payment options.

Uplift: free of charge for travel merchants

Uplift is another US travel-specific solution currently available throughout the United States and Canada. There’s no Uplift app so merchants can only add it as a payment option. This lender currently works with 200+ diverse travel partners including Kayak, United Airlines, Southwest Airlines, and Royal Caribbean.

Besides offering payment flexibility to individual travelers, it’s now accepted for payment by ARC which allows travel agents to process Uplift payments like any ARC Pay transaction using their preferred GDS or ARC Pay Hub via the My ARC portal.

Shopping with Uplift

Commission structure. Uplift also charges interest instead of earning on late (or any other) fees.

Merchant fees. Uplift claims that there are no merchant fees at all.

Integration. Uplift’s pre-integrations include such hospitality and OTA platforms as Revelex, RezMagic, ReservHotel, Intelisys, Softvoyage, and Odysseus Solutions. Access to their Developer portal is granted after registration.

Where to start. To sign in as a partner, fill out the form and go from there.

Some other popular BNPL providers are Afterpay, PayPal Credit, Sezzle, and Zip. However, they are mostly retail-focused and have much fewer travel partners than the ones we described above.

Buy now pay later from ARC, Sabre, and Amadeus

After buy now pay later conquered retail, it became impossible to ignore it. So major travel industry players such as ARC, Sabre, and Amadeus started adding it to their payment processing portfolios. Take a look at what they currently offer and consider collaborating with travel heavyweights.

ARC Pay helps agencies process travel-related payments and, as we mentioned above, partnered with Uplift to offer the buy now pay later service to both ARC-accredited agencies and Verified Travel Consultants (VTCs).To enroll, you’ll have to register with Uplift and take the certification course at the Uplift Learning Portal. See all the detailed instructions at the ARC Pay Hub on My ARC.

Digital Connect API from Sabre is a connectivity solution that gives travel partners access to Sabre technologies and, among other things, helps manage payments. Book Now Pay Later, backed by BNPL lender Zip, is one of the flows that can be incorporated in the airlines' ticketing process, giving flyers an opportunity to put the booking on hold.

Xchange Payment Platform by Outpayce (a wholly owned Amadeus company) partners with hundreds of acquiring banks, payment service providers, and fraud fighters to ensure smooth transaction processing for travel companies. It has recently announced its collaboration with Uplift and Fly Now Pay Later so that airlines, hotels, and other travel businesses can add BNPL options to their sales channels via a single connection to Amadeus.

Maria is a curious researcher, passionate about discovering how technologies change the world. She started her career in logistics but has dedicated the last five years to exploring travel tech, large travel businesses, and product management best practices.

Want to write an article for our blog? Read our requirements and guidelines to become a contributor.