Techtalks: Traveltech

- questions

- answer a question

- sign in

OTA Payment Processing Models and setups

Hi!

I have a question in regards to the Payment Processing models or actual setups that are used by OTAs. I am not talking about Booking.com or Expedia, it's mostly a question of how new and smaller OTAs set up their payment procedures.

For example, when a customer books a trip on the "Random Travel" website, the customer's credit card gets charged by the travel agency and then the payment goes to the actual property or an airline, right?

What are the other options?

And what payment processors can be used by the OTA to charge their customers?

For example, Stripe charges 2.9%+ 0.30c for every transaction, and +1% for every international transaction. This is a lot of money for small OTAs, since the commission is also shared with the Host agency. So if we take an example of a $100 hotel booking, the commission is 10%, in most cases, which is $10. Will say Host agency takes 30% of the commission, that's $3. Stripe takes 2.9% of the entire amount paid, which is another $3.

In the end of the day, the agency is left with $3-4 commission.

So my question is: what are the ways to set up an efficient payment process and what could be the options?

Sorry for the long question. It's really something I am trying to understand.

asked Apr 13, 2020

answered May 8, 2020

Hello Massimo,

Thank you for your interest.

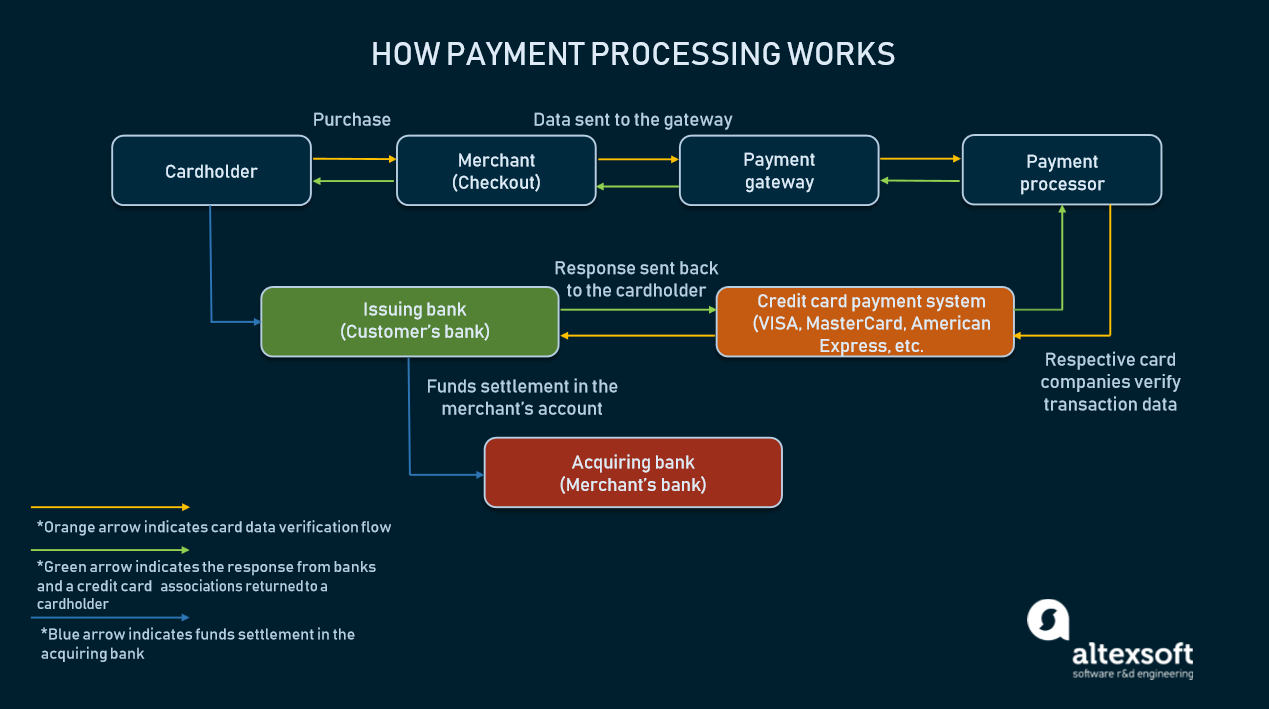

First, let’s unravel the payment processing flow.

You described the business model where a travel agency is accepting direct payments from customers and functions as a merchant of record. Adding a commission to the net-price, an OTA charges the client. Usually, an agency integrates a payment gateway to process payments.

In more detail, payment processing works like this:

When the money is on the agency’s account, it pays the supplier its share. In the case of flights, OTAs must be IATA-accredited to pay airlines directly. Small OTAs aren’t usually certified, so they leverage a consolidator as a payment mediator between them and an airline.

But if an OTA doesn’t function as a merchant, usually, it redirects to a supplier (in case of a direct distribution) or a larger OTA like Expedia or Booking.com for a transaction. According to this business model, OTAs get paid their percentage of the total price at the end of the month. Payment processing isn’t on their shoulders so they don’t owe commissions to payment gateways.

Expedia, for instance, provides EPS Checkout - a white-label solution that collects credit card data and then transmits it to EPS servers where the data is validated and stored.

Distributing hotels, some agencies list the rooms and allow customers only to book but pay already at the property. So that the hotel will pay back the OTA the contracted commission after the check-out.

Your second inquiry was about cost-efficient payment processors.

Setting up a payment gateway is lucrative in case your OTA has a large payment volume:

The more transactions a gateway processes, the less percent it charges per card. Hence, an OTA with about 5000 transactions per month will pay a higher commission per transaction than an OTA with 50000 transactions.

There’s a great number of payment gateways but they offer a similar set of services for a fairly similar price. So, we wouldn’t say that looking for a cheaper payment gateway can save you a lot of money. What really can be a game-changer is negotiating competitive rates and deals with end-product suppliers. Besides leveraging GDS generic deals, it’s necessary to extend your own pool of providers ready to work with you on exclusive conditions. You can read more marketing tips for travel agencies in our article.

All in all, defining a payment processing strategy is a complex task. So, you may want to get in touch with our sales team for further discussion.